Nudging mobile money adoption

A $4.50 Nudge That Changed How Rural Niger Sends Money Home. What a randomized experiment in West Africa tells us about breaking the barriers to mobile money adoption. An opinion piece by Prof. Dr. Michael Grimm.

Imagine sending part of your wages home to a family in rural Niger. The trip from the city is long. The informal agent charges a fee of anywhere between 1% and 30% of whatever you send. And even when the money arrives, it may not arrive on time – or at all. Now imagine doing this every month, for years, while living on a low wage in the first place. This is not a hypothetical scenario. It is the everyday reality for millions of migrant workers across Sub-Saharan Africa, caught in what researchers have called a “double whammy”: poverty drives migration, and punishingly high transfer costs erode the wages earned abroad before they ever reach the people who need them most.

Mobile money, such as M-Pesa in Kenya, promises to change this. The evidence that it can do so is compelling: studies from Kenya, Mozambique, Tanzania and beyond show that mobile money can dramatically reduce transaction costs, smooth consumption in times of crisis, and meaningfully reduce poverty. Yet despite mobile money services existing in Niger since 2009, only around 6% of adults had a mobile money account as recently as 2025. Why is a technology with such clear benefits so underused? And what would it actually take to get people to try it?

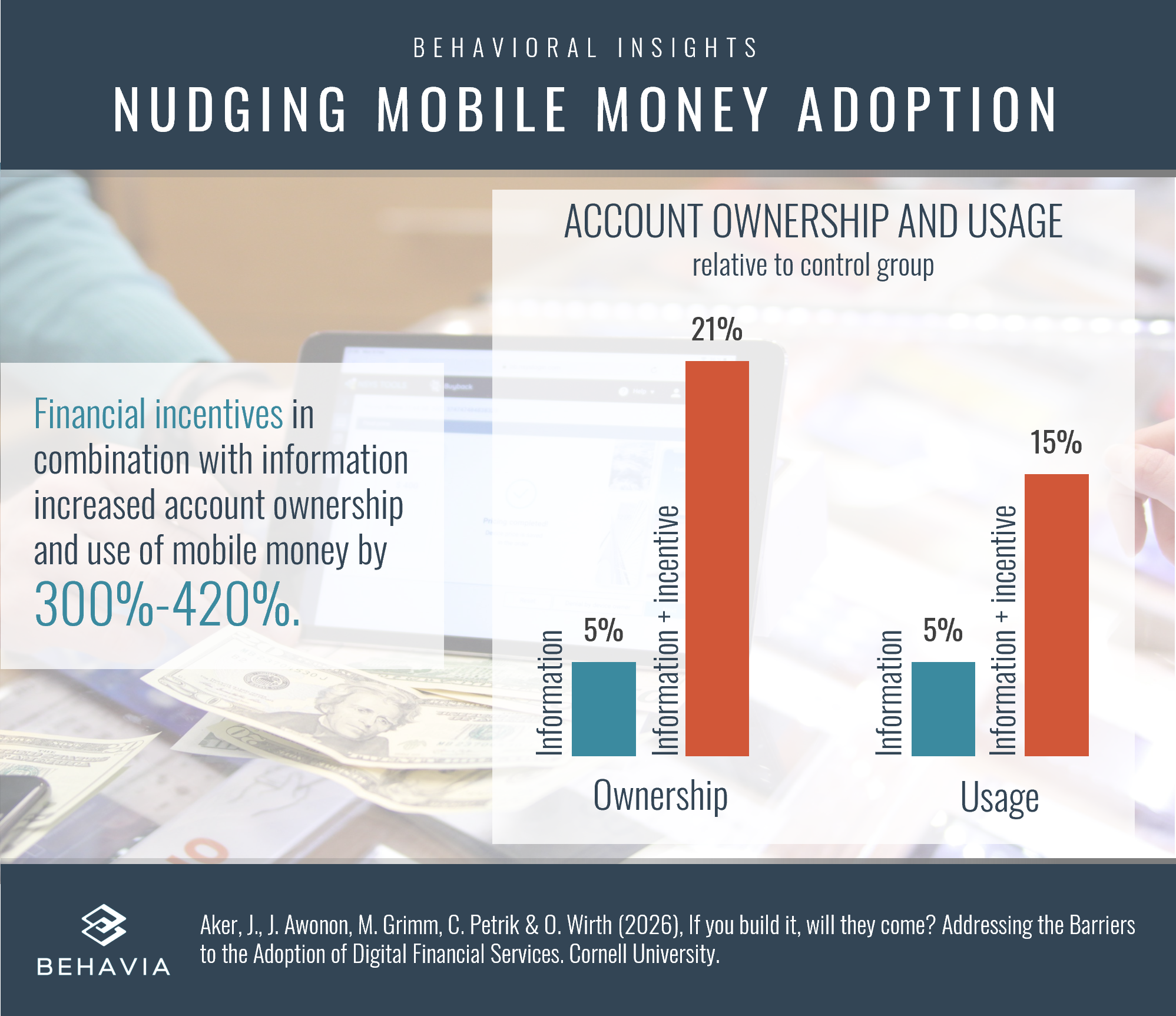

A randomized controlled trial (RCT) conducted across rural villages in Niger set out to answer these questions – and the results are striking. A modest two-sided financial incentive worth just about USD 4.50 in total led to a more than 200% increase in mobile money account ownership, with effects that persisted even nine months after the intervention ended.

The Problem: Knowing Is Not Enough

It is tempting to assume that low adoption of mobile money reflects a lack of information. If people just knew how it worked, the thinking goes, they would use it. But the Niger study challenges this view directly. The experiment tested two distinct interventions in a village-level randomized design across 978 households (337 in a control group, 641 in treatment groups).

The first was a pure information treatment: enumerators visited households, explained how mobile money worked, and provided a printed flyer. The second added a two-sided financial incentive on top of the information: households received 2,000 CFA francs (roughly USD 3) if they received a mobile money transfer within a set window, and the sender received 1,000 CFA francs (roughly USD 1.50), making the total incentive around USD 4.50.

The information-only treatment increased knowledge about mobile money. But it had no measurable effect on actual adoption. People learned about the technology, but did nothing differently. This is a familiar finding in behavioral science: information alone rarely drives behavior change, particularly when adoption involves unfamiliar technology, upfront effort, and uncertain payoffs. Knowing that something is beneficial is not the same as experiencing it.

The Intervention: Making the First Step Cheap and Social

The incentive treatment worked through two reinforcing mechanisms. First, it made trying mobile money cheap and salient. The small cash reward effectively subsidized the first transaction, making “learning by doing” essentially free. People did not need to trust a system they had never used; they were being paid to find out. This is a classic application of behavioral insights: reducing the cost of a first action to overcome inertia and status-quo bias.

Second, the two-sided design, i.e. rewarding both sender and receiver, deliberately targeted network effects. Mobile money is only valuable if the people you want to send or receive money from are also using it. By incentivizing both sides of a transaction simultaneously, the experiment seeded adoption across social networks, not just within individual households. The result was a self-reinforcing dynamic: as more people in a village started using mobile money, it became easier and more natural for others to follow.

Notably, the information treatment also generated meaningful knowledge spillovers within villages: untreated households in information villages showed increased awareness compared to pure control villages. This suggests that information does travel through social networks, even if it does not, on its own, translate into behavior change.

The Results: A Boost to Adoption and Usage That Lasted

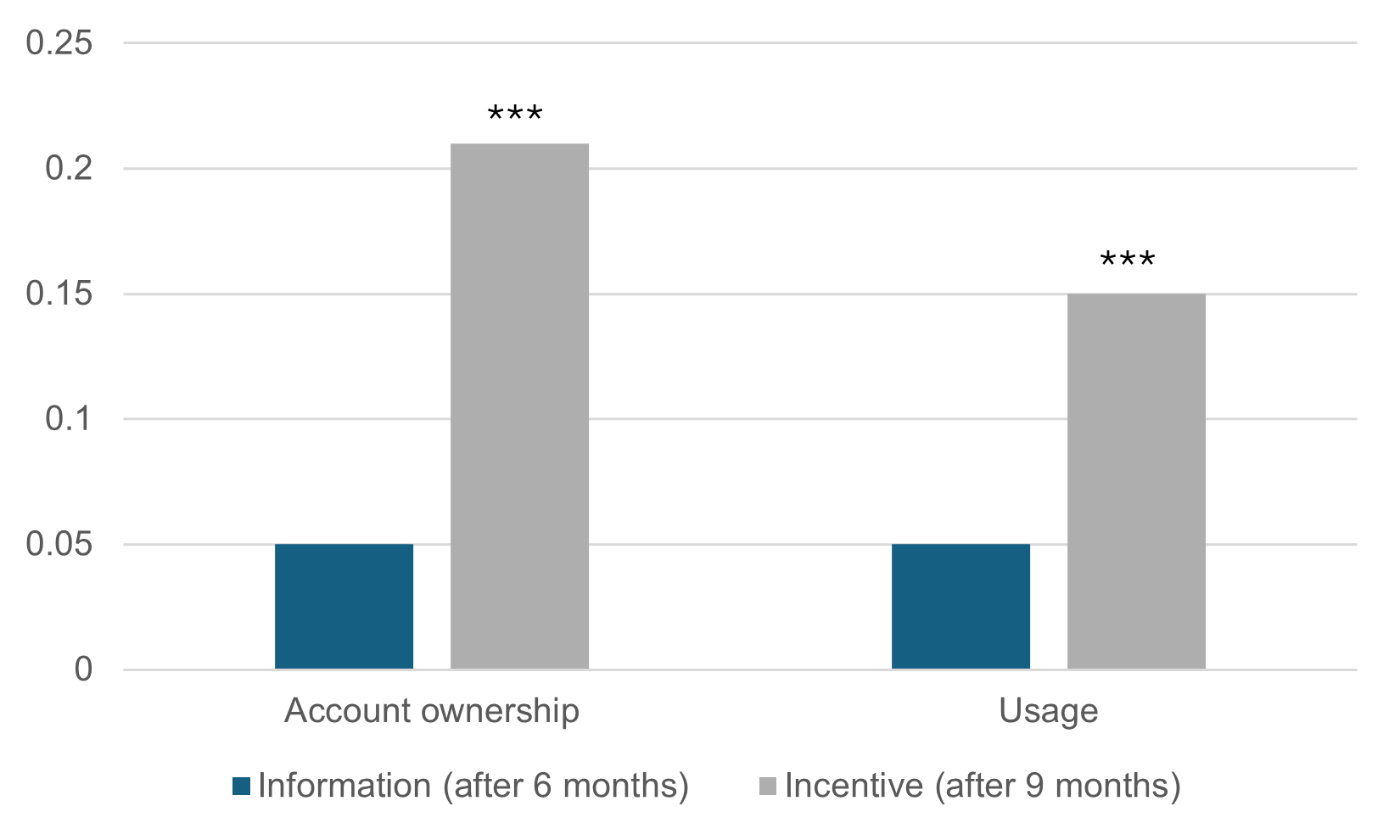

The numbers from the incentive treatment are remarkable. After the intervention, 30% of households in treatment villages held a mobile money account – compared to just 9% in the control group. That is an effect size of over 230%. 20% of households used mobile money and saved via mobile money, an increase of 280% as compared with the control (5%). And crucially, these effects persisted nine months after the intervention had ended, i.e. well beyond the period in which the incentive was active.

On welfare outcomes, the picture is more nuanced. In the short run, no significant consumption-smoothing effects were detected. But over a longer horizon, treated households were more likely to have received a remittance transfer (a 24% increase), and reported higher subjective wellbeing relative to their neighbors. The direction of effects on the number and value of transfers was positive, though not statistically significant, possibly reflecting the short follow-up window relative to the slow-moving dynamics of remittance behavior.

The persistence of adoption is perhaps the most policy-relevant finding. Often, incentivized behavior reverts once the incentive is removed. Here, it did not, suggesting that the intervention succeeded not just in getting people to try mobile money once, but in integrating it into how households manage money.

Effects of information and incentive treatments (relative to control group)

Bars show the share of households having a mobile money account and having used mobile money recently

Notes: *** Effect statistically significant at the 1% level.

Is It Worth It? The Cost-Effectiveness Case

The intervention has a good chance to be cost-effective, both for participants and for policymakers. The total incentive cost per household is modest (roughly USD 4.50), and the downstream benefits – reduced transfer fees, access to formal financial infrastructure, improved consumption-smoothing over time – accumulate. The results imply that the cost of an additional adopter was about 47 USD, this is about 35% less of what comparable interventions have achieved. For mobile network operators and financial inclusion programs, a one-time, low-cost nudge that generates durable adoption should be a compelling investment.

This matters not only for Niger, but for the broader challenge of financial inclusion across Sub-Saharan Africa, where cross-border remittance fees remain among the highest in the world, and where over half the population remains outside the formal financial system despite rapid growth in mobile money infrastructure.

What Policymakers and Practitioners Can Take Away

- Information is necessary but not sufficient. Awareness campaigns can raise knowledge, but they do not reliably change behavior. Policymakers and financial inclusion programs should not mistake information provision for meaningful intervention.

- Small, well-designed incentives can have outsized and lasting effects. A subsidy of around USD 4.50 per household, structured to reward both sender and receiver, produced effects that persisted nearly a year after the program ended. The design matters: two-sided incentives that seed network adoption are likely more effective than one-sided individual rewards.

- Behavioral frictions, not just financial ones, are holding back adoption. The barriers to mobile money use are not primarily about cost or access. They are about the unfamiliarity of a new technology, the absence of a trusted social reference point, and the coordination problem of needing your network to also adopt. Interventions that address these frictions directly, by making first use easy, salient, and social, are more likely to succeed.

- Low-cost behavioral interventions can be a powerful complement to infrastructure investment. Building the infrastructure for mobile money is necessary. But infrastructure alone is not sufficient if behavioral barriers prevent take-up. Pairing infrastructure rollout with targeted, evidence-based behavioral interventions could substantially accelerate financial inclusion outcomes.

References

This opinion piece is based on the following working paper:

- Aker, J., J. Awonon, M. Grimm, C. Petrik & O. Wirth (2026), If you build it, will they come? Addressing the Barriers to the Adoption of Digital Financial Services. Cornell University.

Further readings:

- Aker, J.C., R. Boumnijel, A. McClelland & N. Tierney (2016). Payment Mechanisms and Antipoverty Programs: Evidence from a Mobile Money Cash Transfer Experiment in Niger. Economic Development and Cultural Change, 65 (1): 1-3. https://doi.org/10.1086/687578.

- Batista, C. & P.C. Vicente (2025). Is Mobile Money Changing Rural Africa? Evidence from a Field Experiment. Review of Economics and Statistics, 107(3): 835–844. doi: 10.1162/rest_a_01333.

- Klapper, L., D. Singer, L. Starita & A. Norris (2025). The Global Findex Database 2025: Connectivity and Financial Inclusion in the Digital Economy. Washington, DC. doi: 10.1596/978-1-4648-2204-9.

- Riley, E., A.S. Shonchoy & R. D.Osei (2025). Incentives and Endorsement for Technology Adoption: Evidence from Mobile Banking in Ghana. Journal of Development Economics, 176: 103511. doi: 10.1016/j.jdeveco.2025.103511.

- Suri, T. & W. Jack (2016). The long-run poverty and gender impacts of mobile money. Science, 354(6317) : 1288–1292. doi: 10.1126/science.aah5309.

Prof. Dr. Michael Grimm

Michael Grimm is a Professor of Development Economics at the University of Passau. He is also affiliated with IZA@LISER, the DIW, the RWI Research Network and the Abdul Latif Jameel Poverty Action Lab (J-PAL). He studied in Frankfurt and Paris and earned a PhD at Sciences Po Paris. Before joining the University of Passau, he had positions at the University of Göttingen and the Erasmus University Rotterdam. He was a guest professor at the Paris School of Economics and the University of Bordeaux. He has been a consultant for the World Bank, for various UN agencies, for Dutch, French, and German donor agencies, and for PARIS21 at the OECD.